")

")

“How do I transfer my RRSP from my bank to Wealthsimple?”

Great news for Wealthsimple. Not so great for the banks, but I get how we got here.

As a financial planner who charges fee-for-advice, I don’t have a strong opinion on where you should hold your investments. I do have a few thoughts on where you shouldn’t, but that’s a conversation for another day. What I care about is whether your investment strategy is responsible and whether it actually works.

In my practice, I sometimes manage clients’ investments directly if that’s what they want and it makes sense for their situation. Other times I help them set up self-directed accounts online and offer guidance on portfolios and strategy. Whatever works. The point is, I have no hidden agenda to steer you toward any one platform. I’m here to provide clear, useful information.

But back to the issue: How well does ChatGPT do at answering Canadians’ number one personal finance question of “How do I transfer my RRSP from a bank to Wealthsimple?”

I asked ChatGPT this myself.

Here’s what it got right, what it missed, and how those gaps could quietly cost you hundreds or even thousands of dollars.

So, ChatGPT: How do I transfer my RRSP from my bank to Wealthsimple?

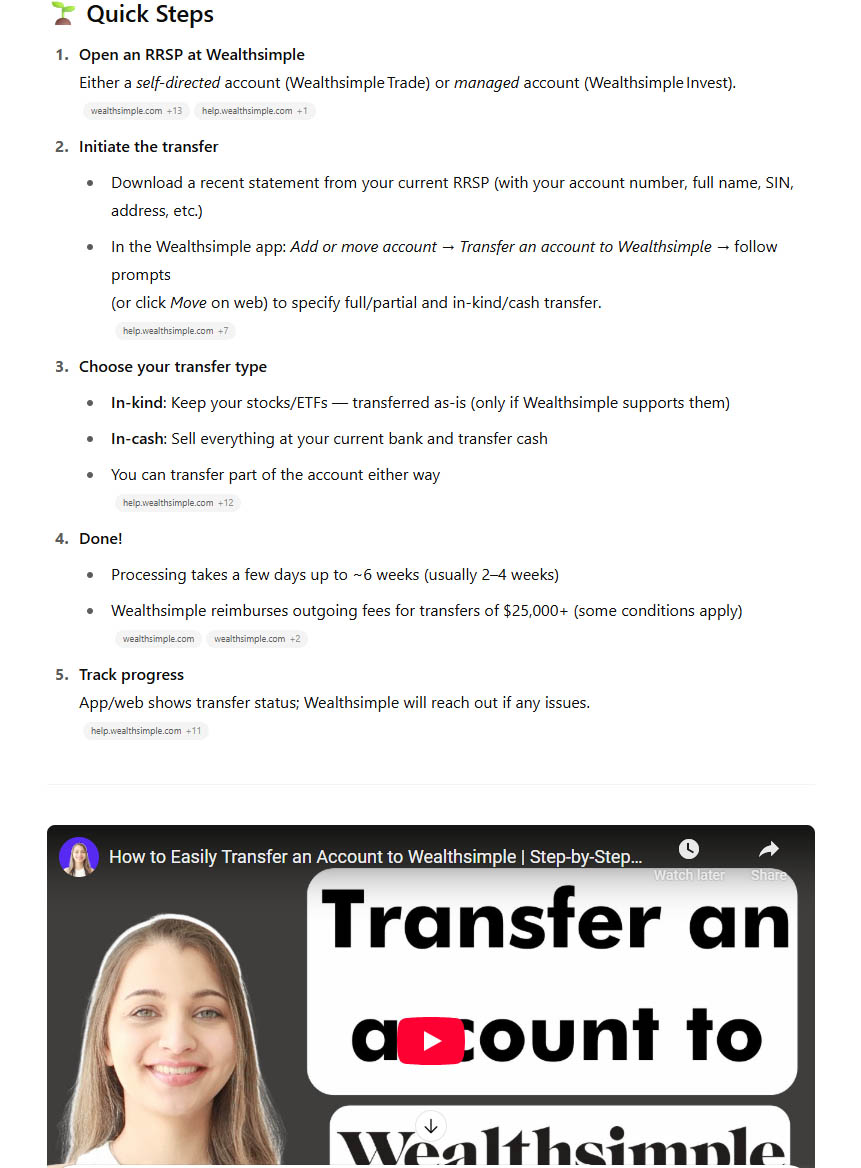

The answer seems pretty straightforward. It took the steps from Wealthsimple’s how-to video, put them in list-format, and even embedded the video for me.

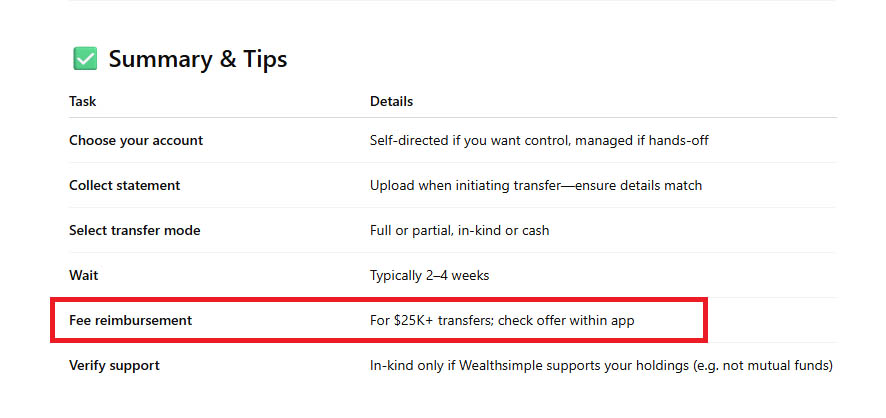

It even included this little reference card to summarize the information.

Sounds good, right? Seems correct. Seems like it covered all the basics.

You know I’m about to throw a wrench in this.

See that part where it says “Fee Reimbursement For $25K+ transfers”? This is where details matter. A lot.

It says to check the offer within the app, so that’s exactly what I did. And if you check it, yes, that is essentially correct, BUT only administrative transfer-out fees are covered. Mutual fund exit trading fees, trading commissions, etc. are not. There’s nothing about any of that in ChatGPT’s information.

What are transfer-out fees, exactly?

In general, transfer-out fees usually range between $50 – $150, which is a small price to pay for Wealthsimple to accumulate $25K plus in assets, if I do say so myself. FYI you have to stay invested with Wealthsimple for 90+ days otherwise they’re allowed to reclaim that fee if you take your money out.

Depending on where your investment is, when you bought it, and what your circumstances were at the time you opened the account, you might have other transfer fees associated with moving your money out. Again, there was nothing in ChatGPT’s instructions about this, but it’s kind of important to know, wouldn’t you say?

Penalty fees you might not even know about

One overlooked fee (and arguably the most significant) is the Deferred Sales Charge (DSC). It’s a penalty fee (generally ranging from 1-7%) that you’ll pay if you sell certain mutual or segregated funds within a set time period, typically 5-7 years from the date the funds were contributed. Let me say that again. It’s not just 5-7 years from when you opened your account. Each contribution you make to any investments under a DSC starts its own holding period clock.

Here’s an example. Say you opened an investment in 2018 with $20,000, and it came with a deferred sales charge (DSC) schedule. On a typical 7-year schedule, you’d pay a 7% fee if you withdrew in the first year, dropping by 1% each year until the fee disappears in 2025.

Now imagine you added another $50,000 in 2020. That deposit starts its own 7-year clock, ending in 2027. So in 2025, even though your original $10,000 is free to move, the $50,000 could still be hit with a 3% penalty. 3% of $50,000 is $1,500. Would you still be in a rush to move your investment if you knew it was going to cost you $1,500?

FYI: DSCs have been banned on new mutual fund contracts since June 2022 and new segregated fund contracts since June 2023. Deposits made before then could still be on a fee schedule.

Depending on the value of your investment, you could pay thousands in fees to move that investment out, and if you relied on ChatGPT’s advice at face value and didn’t dig any further, you’d have no idea what was about to happen.

Oh, and once you move that money out and the fees are charged, it’s gone. You can’t get it back or file a complaint about it.

Some people will keep digging or learn how to check their investment statements to figure out which fees apply. But after all that effort, you’ll still need to call the institution holding your investment to get the exact numbers. You might have been better off making that call from the start and saving yourself the extra work.

And finally, let’s bring in the tax-man.

The risk isn’t just what ChatGPT gets wrong. It’s what you might assume based on what it leaves out.

It makes no mention of taxes, because technically, a direct transfer from one RRSP to another isn’t taxable. But it also doesn’t say, “Make sure you transfer it directly.”

What if you cash it out first, thinking you’ll just move the money yourself? In that case, the full amount is treated as income and taxed.

And what if you asked about your RRSP, but then assumed the same steps apply to all your investments? If you have a non-registered account, following the same instructions could trigger capital gains tax. Depending on how much your investments have grown, that bill could be in the thousands.

For now, you’re still more likely to get complete information from a human who knows what questions to ask and which details matter.

Key Takeaways

ChatGPT covered the basics well. It explained how to transfer an RRSP from one institution to another, mentioned Wealthsimple’s fee reimbursement program, and linked to the full policy.

But it left out some important context.

It didn’t mention potential costs like deferred sales charges on older investments. It also didn’t warn that if you withdraw funds instead of transferring them directly, the full amount is taxed as income. The advice was specific to RRSPs, so it didn’t clarify that other account types follow different rules. Applying the same steps to a non-registered investment, for example, could trigger capital gains tax.

The information wasn’t wrong, it just wasn’t complete. Missing details like these can lead to costly outcomes.

So what should you do?

ChatGPT can be a helpful starting point, but it shouldn’t be your only source. Always confirm the details with your financial institution before taking action.

If you want help understanding your options and avoiding common pitfalls, I’m here to support you. No pressure, no jargon. Just clear, practical guidance focused on your best interests.

More posts are coming soon on how to use tools like ChatGPT more effectively when it comes to your finances. The goal is not to avoid these tools, but to use them wisely.

")

")